PART D IN A NUTSHELL 2018: Initial coverage, donut hole and catastrophic coverage.

Many Medicare beneficiaries often get confused by Part D and rightly so. Below you will find a break-down of your costs associated with Part D; potential exposures, if and when, you are prescribed expensive specialty medication; and a reminder of why it is important to find a broker who rate-shops your medications and plan options each year.

What is Part D

Medicare Part D is a voluntary outpatient prescription drug benefit for people on Medicare that went into effect in 2006. All 59 million people on Medicare, including those ages 65 and older and those under age 65 with permanent disabilities, have access to the Part D drug benefit through private plans approved by the federal government; in 2017, more than 42 million Medicare beneficiaries are enrolled in Medicare Part D plans.

During the Medicare Part D open enrollment period, which runs from October 15 to December 7 each year, beneficiaries can choose to enroll in either stand-alone prescription drug plans (PDPs) to supplement traditional Medicare or Medicare Advantage prescription drug (MA-PD) plans (mainly HMOs and PPOs) that cover all Medicare benefits including drugs.

Is it really voluntary?

Enrollment in Medicare drug plans is voluntary. However, unless beneficiaries have drug coverage from another source that is at least as good as standard Part D coverage (“creditable coverage”), they face a penalty equal to 1% of the national average premium for each month they delay enrollment. When the beneficiary opts to enroll in Part D at a later time, the penalty is attached to the beneficiary’s monthly premium. Beneficiaries will be required to pay the monthly penalty in addition to the monthly part D premium, for life. If you do not have access to credible coverage, we recommend picking up a low cost $17-$20 drug plan to avoid penalties and enrollment restrictions later down the road.

Part D Plan Premiums and Benefits in 2018

According to CMS, the 2018 Part D base beneficiary premium is $35.02, a modest decline of 2% from 2017. Actual Drug Plan monthly premiums for 2018 vary across plans and regions, ranging from a low of $12.60 to a high of $197.

Part D enrollees with higher incomes ($85,000/individual; $170,000/couple) pay an income-related monthly premium surcharge (IRMAA), ranging from $13.00 to $74.80 in 2018 (depending on their income level), in addition to the monthly premium for their specific drug plan. According to CMS projections, an estimated 3.3 million Part D enrollees (7%) will pay income-related Part D premiums in 2018. Please note, beneficiaries can appeal IRMAA and avoid premium surcharges.

What does Part D Cover?

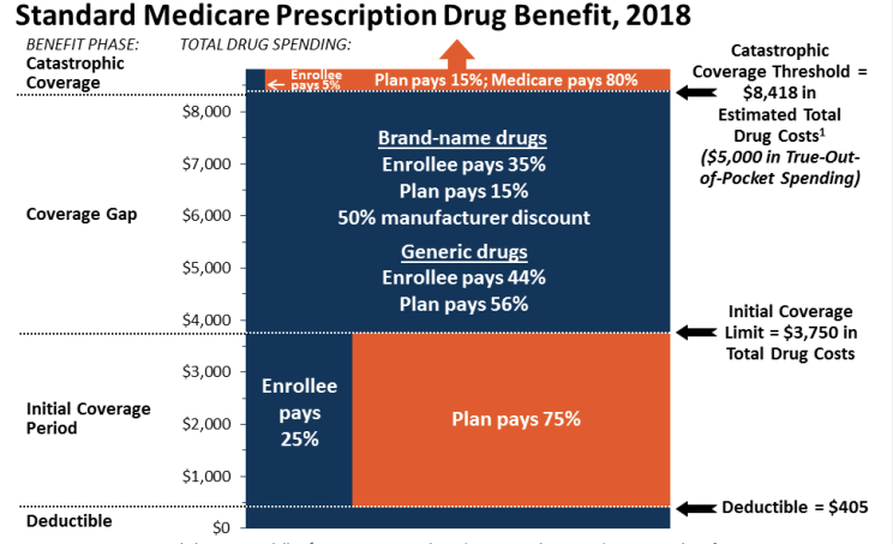

Initial Coverage

In 2018, the Part D standard benefit has a $405 deductible and 25% coinsurance up to an initial coverage limit of $3,750 in total drug costs, followed by a coverage gap, also known as donut hole. During the initial stage, enrollees pay any plan deductible and low copays on filled medications. Once the total retail cost of all filled medications reaches $3,750, the drug plan pushes you into the donut hole.

Example: Enrollee has an inhaler that costs $1,000/month/refill. Of the monthly $1,000 retail value, enrollee’s plan pays $750/month/refill and enrollee pays $250/month/refill. After the fourth month of refills, enrollee’s prescription retail value has reached $4,000. Enrollee has reached/surpassed the initial coverage limit of $3,750. Now the enrollee is in the donut hole/coverage gap where the enrollee’s plan requires her to pay a higher percentage of the cost per medication. Typically, while in the donut hole, enrollees will see their costs increase.

Donut Hole/Coverage Gap

During the coverage gap/donut hole, enrollees are responsible for a larger share of their total drug costs than in the initial coverage period, until their total out-of-pocket spending in 2018 reaches $5,000. In the figure above, all costs highlighted in the dark blue section are payments are used to calculate the enrollees total out-of-pocket spending. Total out-of-pocket spending=deductible + any copayments made by enrollee during the initial coverage stage+ 50% manufacturing discounts + percentage enrollee pays on retail and brand drugs while in the donut hole. Once the enrollee’s total out-of-pocket costs reaches $5,000 for the year, the enrollee is pushed into the Catastrophic coverage phase.

Catastrophic Coverage

After enrollees reach the catastrophic coverage threshold, Medicare pays for most (80%) of their drug costs, plans pay 15%, and enrollees pay either 5% of total drug costs or $3.35/$8.35 for each generic and brand-name drug, respectively. In Catastrophic Coverage, enrollees will generally see significantly lower drug costs.

How Do I Choose a Plan?

Part D plans can (and do) vary in terms of their specific benefit design, cost-sharing amounts, utilization management tools (i.e., prior authorization, quantity limits, and step therapy), and formularies (i.e., covered drugs). Plan formularies must include drug classes covering all disease states, and a minimum of two chemically distinct drugs in each class. Part D plans are required to cover all drugs in six so-called “protected” classes: immunosuppressants, antidepressants, antipsychotics, anticonvulsants, antiretrovirals, and antineoplastics. Plan benefits change annually. It’s critical to review these plans annually during the Annual Enrollment Period, October 15-December 7.

In 2018, most PDPs (63%) will charge a deductible, with 52% of all PDPs charging the full amount ($405). Most plans have shifted to charging tiered copayments or varying coinsurance amounts for covered drugs rather than a uniform 25% coinsurance rate, and a substantial majority of PDPs use specialty tiers for high-cost medications. Two-thirds of PDPs (65%) will not offer additional gap coverage in 2018 beyond what is required under the standard benefit. Additional gap coverage, when offered-mostly with MAPD plans, has been typically limited to generic drugs only (not brands).